Silicon Valley Bank, which catered to many of the world’s most powerful tech investors, collapsed on Friday and was taken over by federal regulators, becoming the largest U.S. bank to fail since the 2008 global financial crisis.

Now, both banks are both under the control of the Federal Deposit Insurance Corporation, or the FDIC.

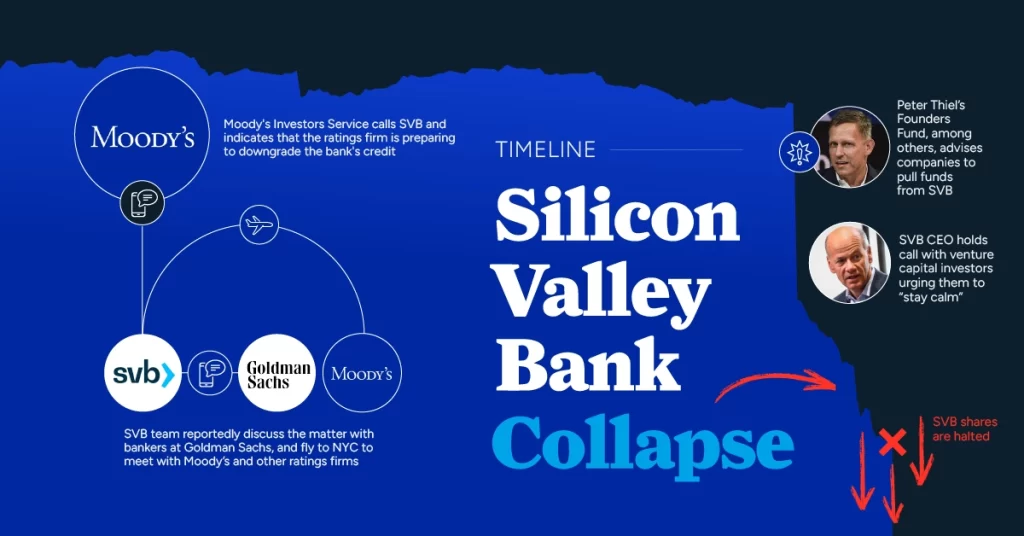

Regulators announced the takeovers after what was effectively a run on Silicon Valley Bank late last week when depositors rushed to withdraw tens of billions of dollars worth of deposits.

The collapse has sent shockwaves across the financial industry. Shares of small, regional lenders have been hammered; the bond market has swung wildly; and now, the pressure is on the Federal Reserve to dial back its interest rate increases even as inflation persists.

What was Silicon Valley Bank?

Although it wasn’t a megabank like Goldman Sachs or JPMorgan Chase, Silicon Valley Bank had punched above its weight during its 40-year history.

Sponsor Message

Based in Santa Clara, Calif., SVB’s clients included venture capital firms, startups and wealthy tech workers. It had become a major player in the tech sector, in which it successfully competed with bigger-name banks.

“They really developed a niche that was the envy of the banking space,” said Jared Shaw, a senior analyst at Wells Fargo. “They are able to provide all the products and services any of these sophisticated technology companies, as well as these sophisticated venture capital and private equity funds, would need.”

Among its clients were tech and tech-adjacent companies like Roku, Roblox and Vox Media. (It turns out that this concentration in the tech sector was key to its demise.) But it remained little known outside of tech circles — until this past week.

Why did Silicon Valley Bank collapse?

Silicon Valley Bank’s business had boomed during the pandemic as tech companies flourished. The bank’s customers filled its coffers with deposits totaling well over $100 billion.

In 2021, when interest rates were at record lows, the cash-rich SVB invested billions of dollars into long-term U.S. Treasury bonds. Those bonds, which are backed by the U.S. government, are generally considered to be safe, modest investments. But they pay out in full only when they’re held to maturity; otherwise, long-term bonds risk losing value if interest rates rise.

Which is, of course, exactly what happened in 2022, when the Federal Reserve began to aggressively raise interest rates in an effort to rein in rampant inflation. Those rate increases hurt the value of government bonds, including those held by SVB.

In order to make good on those withdrawals, SVB had to sell part of its bond holdings at a steep loss of $1.8 billion, the bank said last week. That announcement spooked the bank’s clients, who got worried about SVB’s viability, and then proceeded to withdraw even more money from the bank — a textbook definition of a bank run.

What happens next for people who had ties to SVB?

Federal officials say that all customers of SVB will have full access to their deposits — even accounts that held more than $250,000, the limit of FDIC insurance. Accounts holding greater than that amount made up the vast majority of accounts at SVB. The move essentially guarantees the $175 billion that was in customer deposits at SVB.